My 2025 Jane Street HackerRank Experience With Real Questions

I interviewed for the quant trader role at Jane Street. The Jane Street test had 4 questions with a 30-minute time limit. The overall difficulty was moderate. It didn’t involve complex algorithms, the focus was on probability, expectations, and Bayesian updating, which are core fundamentals in quant trading.

I’m really grateful to Linkjob.ai for helping me pass my interview, which is why I’m sharing my Jane Street OA questions and experience here. Having an undetectable AI assistant for my interview during the OA indeed provides a significant edge.

This article is part of the HackerRank series, and here's how it went for me on the online assessment. If you're interested in other articles in this series, feel free to read: Microsoft HackerRank test, JP Morgan HackerRank test, Stripe HackerRank online assessment.

My Jane Street Online Assessment Questions and Answers

The whole test was four questions in 30 minutes—tight, but doable if you're solid on probability. I've seen people ask about the Jane Street online assessment format a lot, so here's how it went for me: no complex algorithms, no LeetCode-style grinding. Just probability, expectations, and Bayesian reasoning. If you're prepping for quant roles, that's where you should focus.

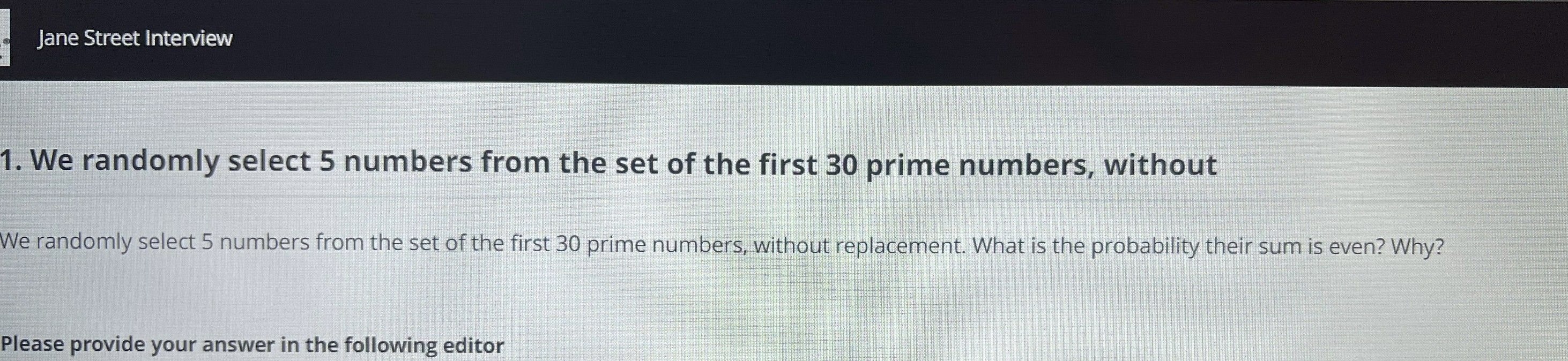

Question 1: Parity of the Sum of Primes

When I first saw the problem, my immediate thought was that the key lies in the parity distribution of prime numbers. After all, whether a sum is odd or even depends entirely on how many odd and even numbers are included.

I started by noting that among all primes, only 2 is even; all the others are odd. Now, if we need to pick 5 primes whose sum is even, the combination must follow the rule “odd number of evens + even number of odds.”

But since there is only one even prime (2), the only possible way to make the total sum even is to choose 1 even + 4 odds. That’s the only combination that works. If we don’t pick 2, then all 5 primes are odd and the sum is guaranteed to be odd, which doesn’t satisfy the requirement.

So the whole approach reduces to: compute the proportion of “5-prime combinations that include 2” out of “all 5-prime combinations.” The key insight is simply recognizing that “2 is the only even prime,” and combining that with parity rules to solve the problem quickly.

Question 2: Dice Game Strategy

This problem is really an optimization question: for each initial roll x, decide whether “stop” or “roll again” gives a higher expected payoff.

My reasoning was: first clarify the payoff rules for each choice.

If I stop, my payoff is just x.

If I roll again, the payoff depends on whether the sum of the two rolls is ≤ 8. If it exceeds 8, the payoff is 0; otherwise, it’s the sum of both rolls.

So the key is computing the expected payoff of rolling again for each x. I list all possible outcomes for the second roll (1–6), compute the resulting payoff for each case, take the average to get E(x), and then compare E(x) with x. If E(x) > x, I roll again; otherwise I stop.

For example, if the first roll is 3, I calculate the payoffs when the second roll is 1–5 (3+y ≤ 8), and note that rolling a 6 gives payoff 0. Then I average these outcomes and compare with 3. The entire strategy boils down to “compute expected value for each x, then choose the higher payoff.”

Question 3: Probability of Heads on the Next Toss

This is a straightforward Bayesian problem: update probabilities based on observed outcomes, then compute the expectation of the next event.

I first organized the given info: there are three coins, A and B land heads 90% of the time, and C lands heads 20% of the time. Initially, each coin is chosen with probability 1/3. Now the first toss is heads, and we want the probability that the next toss is also heads.

My approach has two steps:

Use Bayes’ Theorem to update the probability of having picked A, B, or C, given that the first toss was heads. Since we observed heads, the likelihood of having chosen A or B increases, and the likelihood of C decreases, so we need the posterior distribution.

Compute the expected probability of heads on the next toss using the posterior:

posterior(A) × 0.9 + posterior(B) × 0.9 + posterior(C) × 0.2.

The core idea is: update the initial probabilities based on the observed evidence, then compute the expected probability under the new distribution.

HackerRank is a platform with stringent monitoring measures (including page-switch detection, camera surveillance, and AI behavioral analysis). However, this doesn't mean AI interview assistants can't be used during the interview. Read HackerRank how to cheat to get the answers you want.

Linkjob AI worked great and I got through my interview without a hitch. It’s also undetectable, I used it and didn't trigger any HackerRank detection.

Question 4: Strategy for Drawing from the Urns

This one extends Question 3: not only do we update probabilities, but we must also choose the better strategy. The core is still “Bayesian update + expected value comparison.”

First, clarify the setup: there are two urns, X (mostly $1 chips) and Y (mostly $10 chips). The initial probability of having picked X or Y is 1/2. After drawing a $1 chip, we need to decide whether to “draw again from the current urn” or “switch to the other urn,” choosing whichever gives higher expected value.

Step 1 is the Bayesian update: drawing a $1 makes it more likely that we’re currently holding urn X. So we compute the posterior probabilities: “probability the current urn is X given a $1 draw” and “probability it’s Y.”

Step 2 is computing expected values for both strategies:

For staying, calculate the expectation under the probabilities that the current urn is X or Y, using their remaining chip distributions.

For switching, use the posterior to infer the likelihood that the other urn is Y or X, then compute the expectation based on that urn’s distribution.

Finally, compare the two expected values and pick the higher one. The strategy is simply “update probabilities first, then compute both EVs, then choose the larger.”

What Jane Street Tests in Their HackerRank Assessment?

Based on the test questions and Jane Street’s culture, the core focus areas of its HackerRank assessment can be summarized into the following categories.

Fundamental Math and Probabilistic Thinking

The test focuses on how well I understand and can flexibly apply core mathematical concepts rather than on memorizing complex formulas. It evaluates whether I can quickly extract the key variables in a problem and use number theory, combinatorics, and basic probability to break down uncertainty and build a clear quantitative reasoning framework. The essential goal is to determine whether I possess the kind of fundamental mathematical intuition required in quantitative trading. When facing unfamiliar scenarios, I need to anchor the essence of the problem using basic mathematical logic, which is a necessary foundation for building trading strategies and assessing market probabilities.

Expected Value Analysis and Decision Optimization

This evaluates my ability to make rational decisions in dynamic scenarios by quantifying expected returns. The key is whether I can define the payoff boundaries and risk costs of different choices, compute their expected values, and decide the optimal action instead of relying on intuition. This reflects real-world situations in quantitative trading, such as position management or order placement, where I need to rely on data-driven reasoning to ensure decisions are consistent and logical.

Bayesian Updating and Information Integration

This assesses how I process new information and update probabilities accordingly. It tests whether I can start from an initial assumption, incorporate new evidence, update the probability estimates, and adjust the analytical framework. The core focus is whether I have the ability to perceive changing risks in a dynamic environment. In quantitative trading, market information is constantly shifting, and I must continuously revise strategy parameters and adjust risk expectations using fresh data.

Logical Rigor and Problem Decomposition

This evaluates how I approach complex problems using structured reasoning. It examines whether I can break down an ambiguous problem into quantifiable and analyzable components and proceed step by step through defining variables, building relationships, deriving logic, and validating conclusions. This mirrors the rigor required when implementing trading strategies, where each decision must have a clear justification to avoid losses caused by logical gaps.

Speed and Accuracy Balance

This measures my ability to maintain both speed and precision under time pressure. The test does not require advanced computational techniques, but it expects me to execute basic calculations quickly, simplify analytical models, and avoid careless mistakes while keeping a clear logical flow. This aligns closely with real quantitative trading environments, where markets move quickly and I must assess strategies and adjust parameters within a short time while ensuring decisions remain reliable.

All of these focus areas reflect Jane Street’s goal of identifying candidates who possess the core mindset required for quantitative trading. I need to be able to use mathematical reasoning to quantify uncertainty, rely on data to drive decisions, and use logic to manage risk.

Jane Street Hackerrank Insights and Strategies

Step-By-Step Walkthroughs

When I tackled each Jane Street HackerRank question, I broke the problem into small steps.

For the math sequence: I wrote out each term one by one. I checked my calculations after every step. This helped me spot patterns.

For probability puzzles: I listed all possible outcomes. I counted the cases that fit the question.

Logic puzzles needed a different approach: I started by writing down what I knew for sure. I used elimination to rule out impossible options. I drew quick diagrams or tables on scratch paper.

Mistakes To Avoid

Here are some common pitfalls:

Spending too long on a single question should be avoided.

Using concrete examples to test the logic before submitting an answer improves accuracy.

Filler words should be avoided, and reasoning should be presented in clear, structured steps.

Treating the assessment like a collaborative exercise helps reveal hidden mistakes.

Getting a working solution down first and refining it only if time permits increases efficiency.

FAQ

What is the Jane Street strategy and product online assessment?

I actually didn't get this version—my test was for the quant trader role—but from what I've gathered, the strategy and product online assessment is a variation that leans even harder into game theory and market-making scenarios. The core skills are the same: expected value calculations, probability updates, and quick mental math. If you're applying for a strategy or product role, expect questions that feel like trading simulations rather than pure math puzzles.

Will the Jane Street HackerRank test include problems beyond probability and basic math?

No. The assessment focuses on fundamental quantitative-trading skills and does not involve complex algorithms, programming details, or advanced mathematical derivations.

All questions are framed as practical scenarios and are essentially testing the ability to use basic mathematical tools to reason under uncertainty, which aligns closely with day-to-day quantitative trading work. There is no need to prepare obscure or highly specialized topics.

How to prepare efficiently in the short term if Bayesian updates, expectation calculations, and other core concepts feel unfamiliar?

Short-term preparation can focus on core concepts and question types.

First, strengthen the basics: master Bayes’ theorem (posterior probability calculation), the definition of expected value and its application in decision-making, as well as parity and combinatorial logic, without delving into deep theory.

Next, practice targeted problems such as probability updates, expected value decisions, and combinatorial counting, following the process of breaking down the problem, building a quantitative model, and verifying calculations.

Finally, review the logic: do not dwell on calculation mistakes, but check whether key scenarios were missed, probability update steps are complete, and decisions are based on expected value.

See Also

2026 Nvidia HackerRank Test: Questions I Got and How I Passed

How I Cracked 2026 Citadel HackerRank Assesment Questions

My IBM 2026 HackerRank Assessment: Real Questions & Insights

My 2026 MathWorks HackerRank Assessment Questions & Solutions

Questions I Encountered in 2026 Goldman Sachs HackerRank Test